Are these summer drug price increases hot enough to steal the spotlight from rebates?

The CLIFF NOTES

As a non-profit, we at 46brooklyn have made it our goal to provide insights into U.S. drug pricing data available in the public domain based upon the figures we’ve gathered over the prior month. This month is of course no different, except that you may have noticed drug pricing is one of the hottest topics around again.

One of the reasons this month has been so hot (as it relates to drug prices – not the heat) is that interest in drug rebates are so en vogue again. Some of that is due to the increasingly weird spill-out of the Humira biosimilar market, where PBMs are touting their sainthood for creating protected markets for biosimilars that have list prices that are hundreds of dollars beyond other alternatives. Some of the rebate interest is coming from a recent lawsuit from employers over rebate schemes that created a captive market for brand Tecfidera despite a surge in generic competition (welcome back, Wreckfidera). But the biggest source of rebate interest has to do with diabetes drugs.

Sure, insulins are in the spotlight again thanks to the FTC’s lawsuit against PBMs over the absurd inflation of prices over the past decade despite declines in net costs, but the real belle of the ball for diabetes drugs right now are the glucagon-like peptide-1 (GLP-1) products. GLP-1s are not only one of the biggest medication classes in years thanks to their ability to cause weight loss (upwards of 20+ pounds for some patients), but they are also the latest drug class to take the spotlight in drug pricing conversations (see recent Senate hearings).

Obesity has reached epidemic proportions worldwide and is not just a problem that we face here in the United States. According to the World Health Organization, adult obesity has more than doubled since 1990, and adolescent obesity has quadrupled. To put it more plainly, WHO statistics from 2022 show that one in eight people in the world are living with obesity. Previously (and still existing to some degree depending on who you ask), there has been a stigma around obesity. The American Medical Association classified obesity as a chronic disease more than 10 years ago in June of 2013, however, the actual battle towards this recognition continues to be fought on multiple fronts, with drug pricing at the forefront. For example, prices associated with these GLP-1 weight-loss medication prices are controversial for a number of reasons including drug shortages, formulary coverage, pharmacy reimbursement, compounded products, medical spa practices, and much more.

The list price (but also patient cost share that is tied to list price [i.e., deductibles and coinsurance]) of weight loss medications like Wegovy and Zepbound are what many would consider financially unattainable. Currently, the list price of Wegovy is $1,349.02 per package, and the list price of Zepbound is $1,059.87 per fill. Of course, these are not the net prices of the medicines, nor are they typically the price a patient would pay. But the cost for these weight loss drugs can still be a few hundred dollars for some, especially if they are not covered by insurance. As the cost of these medications continues to be scrutinized by a variety of stakeholders, stay tuned – especially as the next few months progress and we get closer to the Presidential election. We’d expect to see weight-loss medications remain in the hot seat as there are many interested parties who would like to see the cost of these medications come down even further than the current plan Lilly has for Zepbound.

But GLP-1 drug prices cannot have all the spotlight – at least not in this month’s review of August drug price changes – as none of the buzzy GLP-1s have taken a WAC list price change since January 2024. However, other drugs did have.

There were a net 21 brand drug list price increases in August, with price changes ranging from ProQuad on the low end of gross prior year gross Medicaid expenditures (PYME), up to drugs like Enbrel SureClick (where last year Medicaid, expended over $1.3 billion in pre-rebate expenditures). In August, some medications had as low as a 2.9% list price increase, whereas others had an increase of up to 27.4%. Depending on the price of a medication, even a small overall percentage increase could be substantial enough to be thousands or even millions of dollars compounded over time.

There was one medication in August that took a price decrease – Abrilada (one of the now numerous biosimilars for Humira) – which took a decrease of 62.5%. Given the supposed promises large pharmacy benefit managers (PBMs) recently made to Senator Bernie Sanders about not disparaging low-list price products, we look forward to seeing PBM formulary updates that embrace this now-lower priced Abrilada product (especially if Abrilada has a lower list price than some of the affiliated PBM labeled adalimumab products by hundreds of dollars [i.e., Quallent Pharmaceuticals and Cordavis Limited; Nuvalia hasn’t launched yet]).

Some of the biggest and/or most interesting movers to take note of for August 2024 were:

Gardasil suspension for injection (7.0% increase; $1 million PYME)

TEPEZZA powder for solution (3.9% increase; $238 million PYME)

Enbrel (3.0% increase; Mini solution for injection – $183 million PYME; solution for injection – $495 million PYME; SureClick Autoinjector – $1.3 billion PYME)

Abrilada solution for injection (62.5% decrease; n/a PYME)

On the generic side of the coin, year-over-year (YoY) generic oral solid price deflation is at 8.6%.

If you wanted the highlights for the month of August, you have them above. If you’re interested in more of the details, as we continue to approach the spooky time of year, read on for more of what we saw in August 2024.

What we saw from brand-name medications in August

1. A small number of brand drug list price changes

There were a total of 22 brand-name medications that saw wholesale acquisition cost (WAC) price increases and one drug that saw a WAC decrease in August, which is featured and contextualized in our Brand Drug List Price Change Box Score.

Price changes this month ranged from -62.5% to 27.4% and impacted $4.7 billion in prior year gross Medicaid expenditures (PYME). As a reminder, brand price increases in Medicaid are largely held in check thanks to the Medicaid Drug Rebate Program (MDRP), which includes rebate penalties for drug price increases that rise faster than the rate of inflation.

This is one of a number of reasons that solely analyzing brand drug list price changes provides an incomplete picture of what’s really happening with brand manufacturer economics, thanks to the growing lot of opaque rebates, discounts, and giveaways that drugmakers shave off those list prices. But alas, until PBMs, insurers, and rebate aggregators make more granular data on net prices public (which should happen at some point; hopefully whenever Transparency in Coverage rules for drug pricing get finalized / enforced), we’ll continue working with what we’ve got.

2. Brand price trends over time

To help contextualize brand-name drug list price increase behavior, we find it beneficial to review past trends. In comparison to the data from prior months of August, this year seems to line up similarly with August 2023, which had 21 (combined increase and decreases) branded price changes. Looking at past trends, overall, August is a month where there have been consistently a small number of branded price changes.

Figure 1

Source: Elsevier Gold Standard Drug Database, CMS State Drug Utilization Data, 46brooklyn Research

The highest number occurred 11 years ago in August 2013 with 59 net branded price increases, whereas the lowest was six years ago in August 2018, when there were only 13 price increases.

To put it into a more recent perspective, in August 2024, there were a net (combined increases and decreases) of 21 medications, 23 in August 2023, 55 in August 2022, 42 in August 2021, and 14 in August 2020.

Moreover, when further examining our brand drug box score visualization, we continue to see August being the time of year where a small number of changes occur for both brand price increases and brand price decreases.

Of the drugs that took increases so far this year, the median price increase has been 4.5% – a percentage that has been holding steady without much fluctuation. On a weighted basis, using Medicaid data, we see brand increases at 0.9% overall and 1.2% based only on drugs that reported a WAC price change (see Figure 1 or Stat Box #3 & #4 within the dashboard).

3. Brand drug list price changes worth taking note of in August

While we have thus far focused on the aggregate brand picture, next we identify specific brand drugs worth taking note of in a couple different ways. Primarily, we look for medications with a lot of prior year gross Medicaid expenditures (PYME). We next look for drugs with large pricing changes (+/- 10%). And finally, we look for drugs that are interesting to us either because we’ve previously written on them, they’ve recently been in the news, or because we find them of unique clinical value. This month, when looking for these drugs in the brand arena, we found several worth mentioning based upon these reasons:

Autoinflammatory Disease Medications

Abrilada (adalimumab-afzb) is a biosimilar for Humira (that in addition, is also interchangeable with Humira), the historic top-selling drug in the world. Abrilada was approved in 2019 by the FDA and received its interchangeable designation in 2023. This drug has the distinction of being the only brand to take a price decrease in August; decreasing by more than 60% of its WAC price (whether biosimilars are categorized appropriately as brands is perhaps something we should update next year). We point out that although this now makes Abrilada cheaper (based upon list price) than most other biosimilar Humira products (including say those of Quallent Pharmaceuticals and Cordavis Limited), we cannot help but notice its absence from say Express Scripts’ National Preferred or CVS’ Value Formulary. We bring this up only because these same PBMs recently gave Senator Sanders assurance they would welcome lower list price GLP-1s. As a result, we wonder if and when that hypothetical will extend to reality with lower priced Humira products (even if it is a competitor to their own affiliated products).

Enbrel (etanercept) is an injectable medication indicated for a variety of types of arthritis, as well as ankylosing spondylitis and plaque psoriasis. It has multiple dosage forms (solution, mini solution (aka prefilled cartridge), and SureClick autoinjector), each of which took a 3.0% increase in WAC, impacting almost $2 billion in collective PYME.

Thyroid Eye Disease

Tepezza (teprotumumab) is indicated for the treatment of Thyroid Eye Disease. It took a 3.9% WAC increase, impacting $238 million in PYME.

Cancer Prevention

Gardasil (Human Papillomavirus 9-valent Vaccine, Recombinant) is a vaccine that helps protect individuals ages 9 to 45 against the following diseases caused by 9 types of HPV: cervical, vaginal, and vulvar cancers in females, anal cancer, certain head and neck cancers, such as throat and back of mouth cancers and genital warts in both males and females. This product saw an increase in WAC of 7%, which results in an additional $1 million in gross prior year Medicaid expenditures (PYME).

Of course, our update doesn’t end with brand medications. While brand drugs represent the majority of payer costs, patients overwhelmingly take generic medications, which means we cannot overlook what is going on with them.

What we saw from generic medications in June

4. A unfavorable, unweighted price change picture

Each month, we start our evaluation of generic drug price changes by looking at how many generic drugs went up and down in the latest month’s survey of retail pharmacy acquisition costs (based on National Average Drug Acquisition Cost, NADAC), and compare that to the prior month. Basically, the quick way to read Figure 2 below is to look for orange bars that are taller than blue bars to the left of the line, and exactly the opposite to the right of the line. That would indicate a good month – more generic drugs going down in price compared to the prior month, and less drug prices going up.

Figure 2

Source: Data.Medicaid.gov, 46brooklyn Research

When you look at Figure 2, on the left side, you can see that the blue bars (which represent July 2024) are much higher than the orange bars (which represent August 2024). However, on the right-hand side, you can see that the blue bars are much shorter than the orange bars. So, in August, you can see that there were not a substantial amount of decreases in generic costs compared to July. Not a good early sign for August generic drug deflation.

For every generic drug that increased in price last month, 0.13 decreased in price. This is almost the exact inverse of what happened in July, where we saw for every generic drug that increased in price 7.4 decreased in price. This is a huge difference to what we are used to seeing in in this area, which typically hovers around ~1.75, give or take a few decimal points.

But as usual, take this unweighted price change analysis with a grain of salt. To really make heads or tails of all of these pricing changes, let’s weight these changes.

5. Weighted Medicaid generic drug costs come in at $618 million inflation

While you can track each individual drug’s NADAC over time at our NADAC Drug Pricing Dashboard, the purpose of our NADAC Change Packed Bubble Chart is to apply utilization (drug mix) to each month’s NADAC price changes to better assess the impact. So rather than treating each price change equally, here, we use detailed Medicaid spending data to weight the price changes relative to the degree with which they are paid for. CMS just published Q4 2023 Medicaid State Drug Utilization Data (SDUD), so we’ve moved to 2023’s full Medicaid drug mix to arrive at an estimate of the total dollar impact of the latest NADAC pricing update. As a reminder, we’re choosing the last full-year picture available in order to remove variances in drug mix from this equation (and focus just on the role that NADAC price changes have over time). This helps quantify what should be the real effect of those price changes above from a payer’s perspective (in our case Medicaid; individual results will vary). So, if a drug that is hardly ever utilized takes a 50% decrease, it doesn’t matter as much if a drug everyone takes increases by 5% (the inverse of this is what we observed at the start of the year with the brand name insulin price decreases [see our January 2024 report]).

The green bubbles on the right of the Bubble Chart viz (screenshot below in Figure 3) are the generic drugs that experienced a price decline (i.e. got cheaper) in the latest NADAC survey, while the yellow/orange/red bubbles on the left are those drugs that experienced a price increase. The size of each bubble represents the dollar impact of the drug on state Medicaid programs, based on their utilization of the drugs in the most recent trailing 12-month period (i.e. bigger bubbles represent more spending). Stated differently, we simply multiply the latest survey price changes by aggregate drug utilization in Medicaid over the past full year, add up all the bubbles, and get the total inflation/deflation impact of the survey changes.

Figure 3

Source: Data.Medicaid.gov, 46brooklyn Research

Overall, in August, there was almost $650 million worth of inflationary drugs, with a super small offset of $31 million of deflationary generic drugs, netting out to a whopping $618 million of generic drug cost inflation for Medicaid.

The month-over-month increase bubble chart is gargantuan compared to its counterpart, which is the exact opposite of what it looked like last month. So, for the month of August, generic drug costs increased substantially whereas in July, generics were decreasing in price. And look, we get it it, these NADAC swings can make you wonder just how ‘good’ NADAC is (see our prior discussion on NADAC’s recent “volatility.” And while we cannot say for certain what is driving all these swings (though we have a good hunch that it’s inconsistent pharmacy data reporting), if we take a step back and look at all months contextualized in the NADAC packed bubble chart (which goes back to March 2024), we can see that NADAC has deflated by over $232 million collectively since March (Figure 4 below).

Figure 4

Source: Data.Medicaid.gov, 46brooklyn Research

Basically, if we give up a little NADAC deflation in one month to some NADAC inflation the next (like we’re doing here; yes $600 million is little in the grand scheme of Medicaid’s $92 billion gross spending), we’re still marching downward on drug costs with NADAC.

And while month-over-month changes are interesting (even when we attempt to look back a few months), they inevitably lead to questions about how year-over-year (YoY) is trending, which leads us to our next analysis.

6. Year-over-year generic oral solid deflation 8.6%

Ever since June 2020, we have been tracking year-over-year (YoY) deflation for all generic drugs that have a NADAC price. We once again weight all price changes using Medicaid’s drug utilization data. This month, deflation on oral solid generics and all generics was at 8.6% and 10.6%, respectively (Figure 5). If you are a purchaser of generic drugs, this deflation is ideal, as it means costs to purchase are declining.

Figure 7

Source: Data.Medicaid.gov, 46brooklyn Research

7. Top/notable generic drug decreases

Although there are not many generic drug cost decreases this month, there are still some interesting ones. Some of the biggest decreases are the nonsteroidal anti-inflammatories (NSAIDs), which can be used to treat acute pain and include lofena, meloxicam, and diclofenac potassium, that each took a decrease of -14.8%, -12.7%, and -14.8% respectively. It is worth noting that in the prior month, meloxicam increased by 21.1%.

Another interesting decrease is propranolol, a beta-blocker than can be used for high blood pressure and a few other indications like performance anxiety disorder or migraine prevention, which took a decrease of -27.1%.

We are also continuing to see ADHD medications decreasing in price this month with dexmethylphenidate ER 5 mg cap decreasing by -42.4%, as well as lisdexamfetamine 60 mg and 40mg capsules decreasing respectively by -6.5% and -12.8%. We also saw methlyphenidate LA 10 mg capsules decrease by -20.8%.

Mercaptopurine 50 mg tablet (AKA 6-MP) is a medication used to treat a variety of conditions including Crohn’s disease and ulcerative colitis; it decreased this month by -33.4%. It is worth noting that the same medication increased by 39.9% in July.

Surprisingly, many of this month’s decreases were actually last month’s increases. For example, propanolol increased by 43.8% in July and nowin August we see that it is coming down in price with a decrease of 27.1%, which is a still a net increase of 16.7%. Meloxicam and 6-MP were also amongst those that increased in July but decreased in August. Quetiapine increased in last month’s report by 22.9% and decreased in August by -17.1% for a net increase of 5.8% across the two months.

8. Top/notable generic drug increases

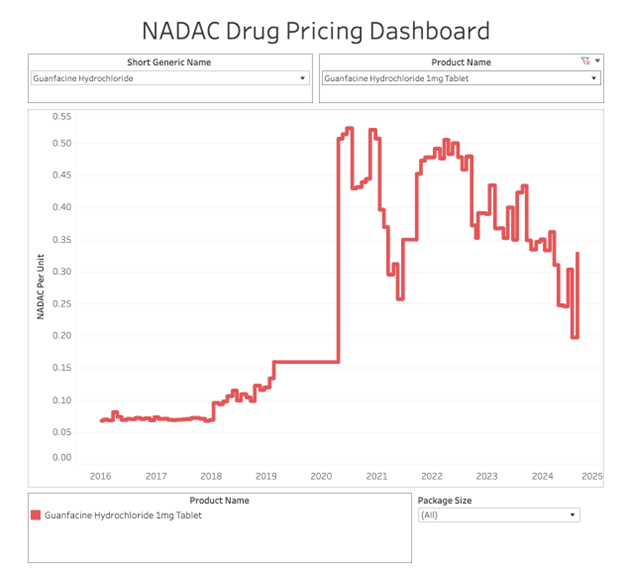

On the increase side of things, the most impactful increases of 50% or above were guanfacine 1 mg tablet (66.5% increase), guanfacine 2 mg tablet (61.2% increase), dextroamphetamine-amphetamine ER 10 mg capsule (63.7% increase), paliperidone ER 9 mg tablet (65.2% increase), trazodone 300 mg tablet (68.9% increase), and methylphenidate LA 20 mg capsule (60.7% increase).

Guanfacine 1mg tablet is a recent repeat offender for us here at 46brooklyn, as we wrote about them a few months ago in our April 2024 article when they came in with a 14% decrease in price.

That’s all for this month! Come back next month to see what kind of spooky activity drug prices get up to.

Thanks to Matt Stoller at BIG for including our money from sick people chart in his recent rundown of the FTC’s lawsuit against PBMs over the inflated prices for insulins.

Shout-out to Brian Reid at Cost Curve for including our dissection of “The Carlton Report” of Express Scripts vs FTC fame in his newsletter.

Lastly, thanks to Suzanne King at the Missouri Beacon for referencing us in her recent news story on another independent pharmacy that has unplugged from the insurance-based system as a mechanism to better control their destiny and lower drug costs for consumers.